All Categories

Featured

Table of Contents

The are entire life insurance coverage and global life insurance. The money value is not added to the death advantage.

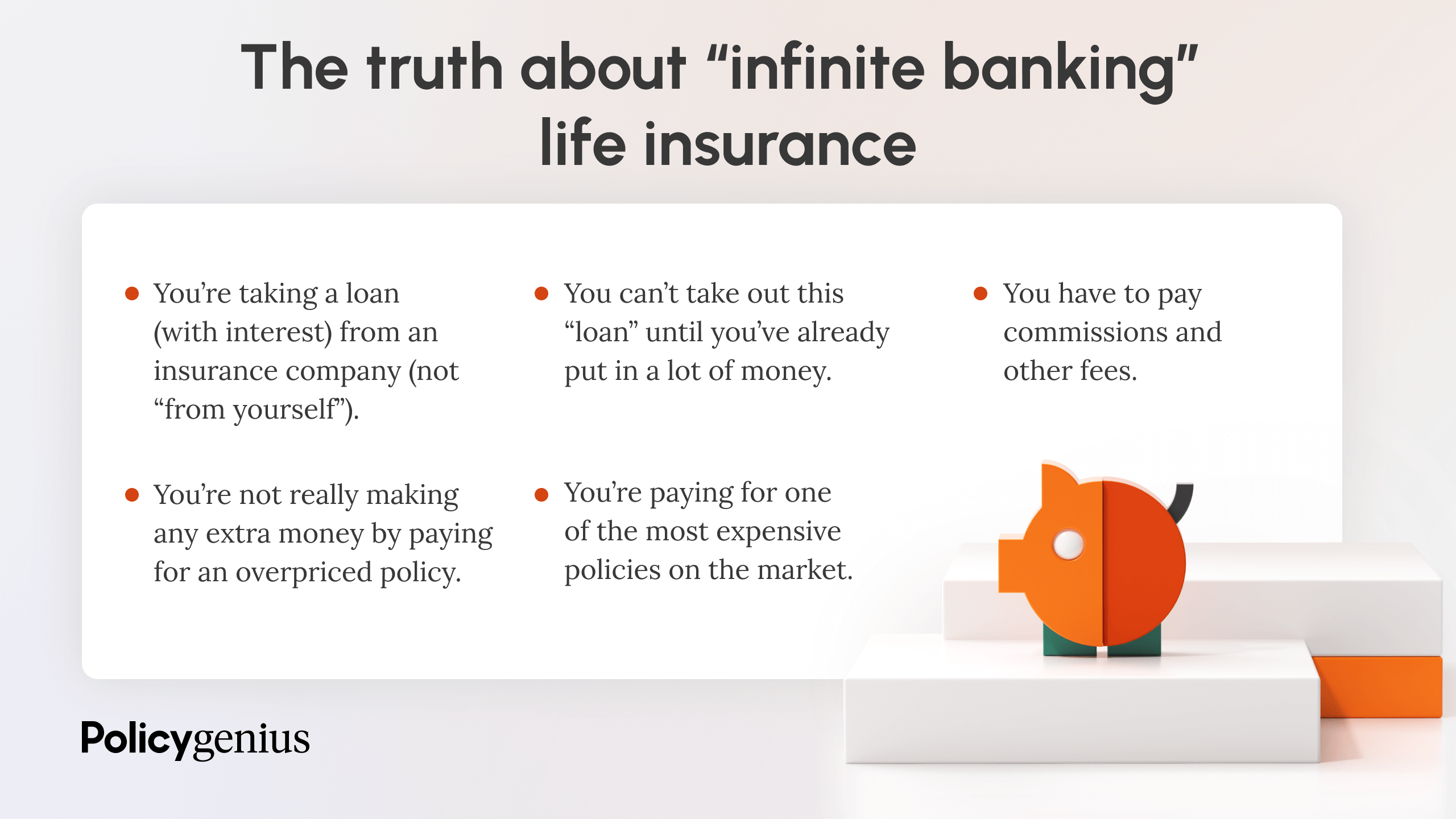

After ten years, the cash worth has grown to about $150,000. He gets a tax-free funding of $50,000 to begin an organization with his brother. The plan lending rate of interest is 6%. He pays off the funding over the next 5 years. Going this course, the passion he pays returns into his policy's cash money value rather than a banks.

Imagine never having to worry about bank lendings or high passion prices once more. That's the power of limitless financial life insurance coverage.

There's no collection finance term, and you have the freedom to pick the repayment schedule, which can be as leisurely as repaying the finance at the time of death. This flexibility includes the maintenance of the loans, where you can select interest-only settlements, keeping the lending equilibrium level and workable.

Holding cash in an IUL dealt with account being attributed interest can commonly be much better than holding the money on deposit at a bank.: You've constantly imagined opening your own bakeshop. You can borrow from your IUL policy to cover the first expenses of renting out an area, acquiring devices, and employing team.

How Do You Become Your Own Bank

Individual lendings can be acquired from conventional financial institutions and lending institution. Below are some vital factors to think about. Charge card can offer a flexible means to borrow cash for extremely short-term durations. However, borrowing money on a bank card is typically very expensive with interest rate of passion (APR) commonly getting to 20% to 30% or more a year.

The tax obligation treatment of plan loans can differ significantly depending on your nation of home and the particular terms of your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan car loans are usually tax-free, using a substantial advantage. In other jurisdictions, there might be tax effects to think about, such as potential tax obligations on the funding.

Term life insurance policy just supplies a fatality benefit, without any type of cash money worth accumulation. This implies there's no money value to borrow versus.

Infinite Banking Canada

When you first find out about the Infinite Banking Concept (IBC), your first reaction may be: This sounds as well great to be real. Perhaps you're skeptical and think Infinite Financial is a fraud or scheme - infinite banking concept explained. We want to establish the document right! The trouble with the Infinite Financial Principle is not the idea yet those persons using a negative review of Infinite Financial as a principle.

So as IBC Authorized Practitioners via the Nelson Nash Institute, we thought we would certainly respond to some of the leading questions people search for online when finding out and comprehending every little thing to do with the Infinite Banking Principle. What is Infinite Banking? Infinite Banking was produced by Nelson Nash in 2000 and totally described with the publication of his publication Becoming Your Own Banker: Open the Infinite Financial Idea.

How Infinite Banking Works

You assume you are coming out economically in advance due to the fact that you pay no passion, but you are not. With conserving and paying cash money, you may not pay rate of interest, yet you are using your money as soon as; when you invest it, it's gone permanently, and you offer up on the possibility to make lifetime compound interest on that cash.

Also financial institutions use entire life insurance coverage for the same purposes. The Canada Revenue Firm (CRA) also acknowledges the worth of getting involved entire life insurance as a distinct asset class made use of to produce long-term equity safely and predictably and provide tax obligation benefits outside the range of standard financial investments.

Infinite Banking Link

It permits you to produce riches by satisfying the banking feature in your very own life and the ability to self-finance major way of life purchases and costs without interrupting the substance rate of interest. One of the easiest means to think of an IBC-type participating whole life insurance coverage plan is it approaches paying a mortgage on a home.

When you borrow from your getting involved entire life insurance coverage policy, the cash money value continues to expand nonstop as if you never obtained from it in the first area. This is because you are making use of the cash money worth and fatality benefit as collateral for a lending from the life insurance policy firm or as collateral from a third-party lender (recognized as collateral borrowing).

That's why it's important to collaborate with a Licensed Life Insurance Broker accredited in Infinite Financial that frameworks your participating whole life insurance policy plan properly so you can stay clear of negative tax ramifications. Infinite Financial as a monetary strategy is except everybody. Right here are several of the pros and cons of Infinite Banking you should seriously consider in choosing whether to move on.

Our recommended insurance service provider, Equitable Life of Canada, a mutual life insurance company, specializes in taking part whole life insurance policy plans specific to Infinite Banking. Additionally, in a shared life insurance company, insurance holders are thought about company co-owners and receive a share of the divisible surplus generated each year through returns. We have a selection of providers to pick from, such as Canada Life, Manulife and Sunlight Lifedepending on the demands of our customers.

Please also download our 5 Leading Questions to Ask An Unlimited Financial Agent Before You Hire Them. To find out more about Infinite Banking see: Disclaimer: The product offered in this e-newsletter is for educational and/or academic functions only. The info, point of views and/or sights expressed in this newsletter are those of the writers and not always those of the distributor.

Infinite Bank

Nash was a financing expert and follower of the Austrian school of economics, which advocates that the value of items aren't clearly the result of standard financial frameworks like supply and demand. Rather, individuals value money and goods in different ways based on their financial status and needs.

One of the risks of standard banking, according to Nash, was high-interest prices on finances. As well lots of individuals, himself consisted of, got into economic problem due to dependence on banking institutions.

Infinite Financial needs you to own your monetary future. For ambitious individuals, it can be the finest monetary device ever. Below are the advantages of Infinite Banking: Arguably the solitary most valuable facet of Infinite Financial is that it improves your cash flow.

Dividend-paying entire life insurance coverage is very reduced risk and provides you, the insurance holder, a fantastic deal of control. The control that Infinite Financial provides can best be grouped right into two groups: tax benefits and possession protections.

Whole life insurance coverage plans are non-correlated possessions. This is why they work so well as the economic structure of Infinite Banking. Regardless of what occurs in the market (stock, real estate, or otherwise), your insurance coverage policy maintains its well worth.

Whole life insurance is that third bucket. Not just is the price of return on your whole life insurance plan assured, your fatality benefit and premiums are also assured.

How To Be Your Own Banker

This framework lines up completely with the principles of the Continuous Wide Range Technique. Infinite Financial attract those seeking better economic control. Here are its major benefits: Liquidity and accessibility: Policy loans offer immediate access to funds without the constraints of standard small business loan. Tax obligation effectiveness: The cash worth expands tax-deferred, and policy finances are tax-free, making it a tax-efficient device for constructing wide range.

Possession protection: In numerous states, the cash worth of life insurance policy is protected from creditors, adding an extra layer of monetary protection. While Infinite Banking has its benefits, it isn't a one-size-fits-all remedy, and it features substantial disadvantages. Below's why it might not be the very best method: Infinite Financial typically requires complex plan structuring, which can perplex policyholders.

{kind=link}

Latest Posts

Cash Flow Banking With Life Insurance

How Infinite Banking Works

Bank On Yourself Reviews